Investment Property Loans: Financing Strategies 2024

Category Investment

Investment Property Loans: Financing Strategies 2024

Investment Property Loans: Are you looking to make money from property investment but feel stuck on how to get the funds? You're not alone.

Many people want to invest in properties to earn rental income, but finding the right loan can be difficult.

We'll cover various loan options, what lenders look for, and strategies for getting more properties under your belt-even if you already have a mortgage. Ready to turn your property investment dreams into reality? Keep reading!

Key Takeaways

- Investment properties can provide steady income and increase in value over time, making them a smart financial move.

- There are several investment property loan options available for investors, including conventional mortgages, hard money loans, private lending, and home equity. Each has different requirements and benefits.

- Understanding the terms of your loan is crucial for success in real estate investment. Strategies like leveraging home equity or refinancing existing loans can help grow.

Understanding The Basics

These properties can turn into a steady source of income if you choose wisely. Think about buying houses or commercial spaces that people will want to rent.

A good property attracts reliable tenants and increases the property's value over time. I learned this firsthand when I invested in a small apartment complex near a university. The demand there stays high, making it a good move.

Before putting your money down, understand all costs involved, not just the purchase price. Expenses like property taxes, insurance, and upkeep eat into your profits. Also, getting familiar with different loan types helps you find financing that fits your needs without breaking the bank on interest rates.

From my experience, taking the time to learn about these basics before diving in makes all the difference between a successful investment and an expensive lesson.

The Advantages of Acquiring Investment Properties

Owning properties adds an extra stream of earnings, which means you get more monthly money from your tenants. As a property owner, you also stand to gain from the increase in your property's value over time.

This growth can significantly boost your wealth and financial freedom.

Getting a property manager can cut down on the work you need to do yourself. They handle daily tasks and problems, making life easier for you as an investor. Plus, being aware of all costs upfront helps avoid surprises later on.

But remember, renting out properties comes with its own set of challenges like laws that protect renters. Yet, these hurdles don't outweigh the benefits - more income, potential profits from value increases, and less personal management hassle make it a smart choice for investors looking to expand and secure their financial future.

Overview of Loan Options

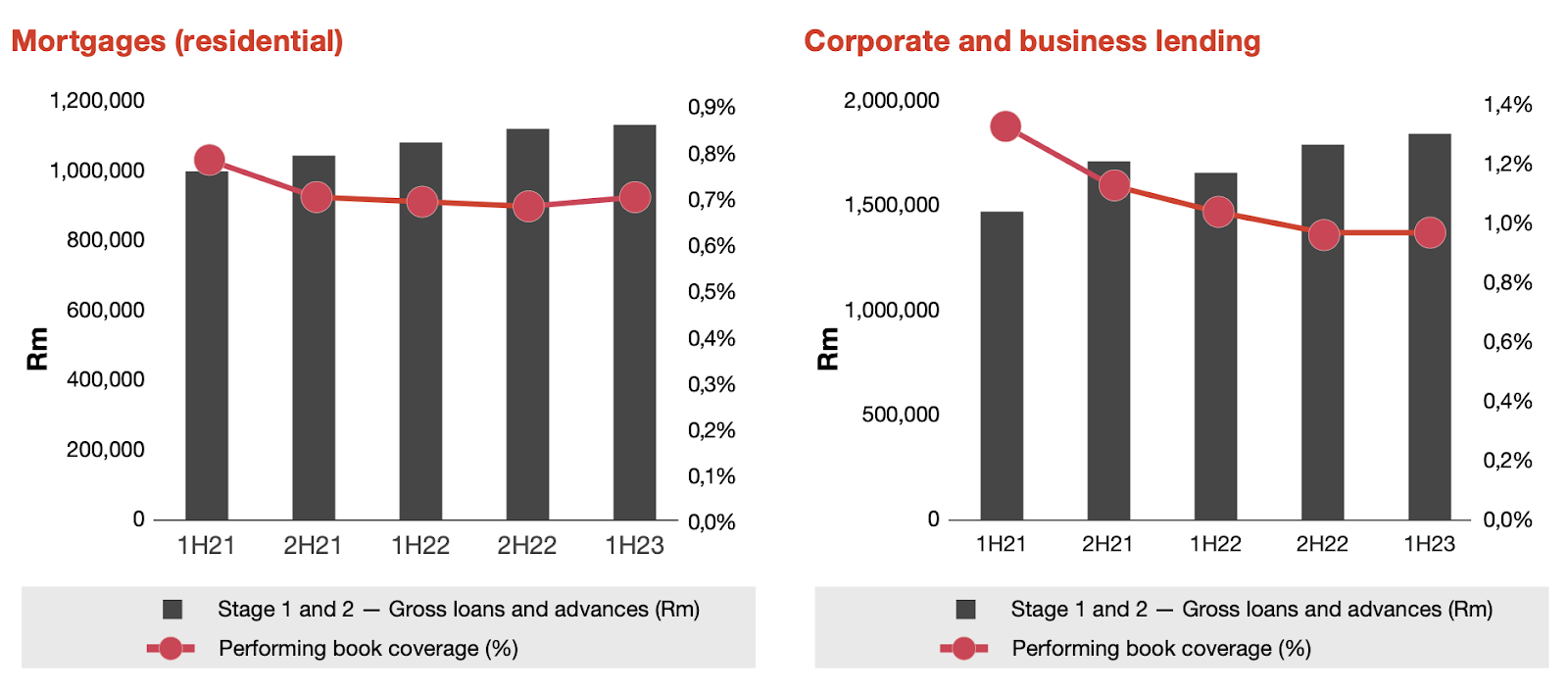

Source: PwC analysis

- In 1H23, performing book coverage levels increased across nearly all loan portfolios as credit models sensitive to economic conditions incorporated the effect of the challenging economic outlook, while individual customers and portfolios of business in certain lending categories migrated between IFRS 9 stages.

- Specifically, interest rate-sensitive retail portfolios including home loans, vehicle and asset finance, and personal unsecured lending - all showed steep increases in coverage levels against the backdrop of the elevated interest rate environment.

Exploring your options for investment property loans opens up a world of possibilities, from traditional bank mortgages to more creative financing solutions like private lending or using your home's equity.

This step is crucial in building your real estate portfolio. Keep reading to find out how you can fund your next property investment with the right loan option for you.

Conventional Mortgage Options

Conventional mortgages are a solid path for real estate investors. They let you buy properties with as little as 3% down. You need good credit and a stable income to qualify. Banks or lenders give these loans without backing from the government.

This means you have more options in what property to buy and how much to spend.

Mortgage interest rates on these loans can change, affecting your payments and how much rent you charge. Always check the latest rates before making a decision, The South African Reserve Bank sets rules for these mortgages, making sure there's a standard in lending practices across the board.

Exploring Hard Money Loans

Hard money loans focus on your future property's earning power, not just your past credit or how much you earn. These loans come from investors or firms that lend based on the value and potential of the real estate you want to buy.

This option works well if you're eyeing a house to flip or a rental property that needs fixing up.

Terms are often shorter, and rates higher compared to bank loans. But don't let that deter you-they can be a powerful tool for getting into real estate investing quickly.

Navigating Private Lending

Exploring private lending means talking directly to people with money to lend. You won't deal with banks or big companies here. Instead, you talk one-on-one with someone willing to invest in your plans.

This path lets you explain why your investment is a good bet, even if your credit score isn't perfect. I once secured a loan this way, despite having a less-than-ideal financial history at the time.

Terms and conditions can vary widely with private lenders compared to traditional loans from banks. Make sure to compare different offers carefully. Private loans might come faster and require less paperwork but watch out for higher interest rates or fees that could surprise you later on.

Always ask about every detail before you agree - it saved me more than once from making costly mistakes.

Utilizing Home Equity for Investment

You have built up equity in your home. Now, think about using that equity to invest in another property. This can be a smart way to generate more income by renting the new property.

You can get a home equity loan or open a line of credit based on the value of your current home. This money acts as funding for your next investment.

I did this myself a few years ago, I used a cash-out refinance on my primary residence to buy a property in Cape Town. My lender looked at how much my house was worth and how much I still owed on it.

Then, they gave me part of this difference as a loan, which I then used as a down payment. Since then, it has been paying off both properties' mortgages.

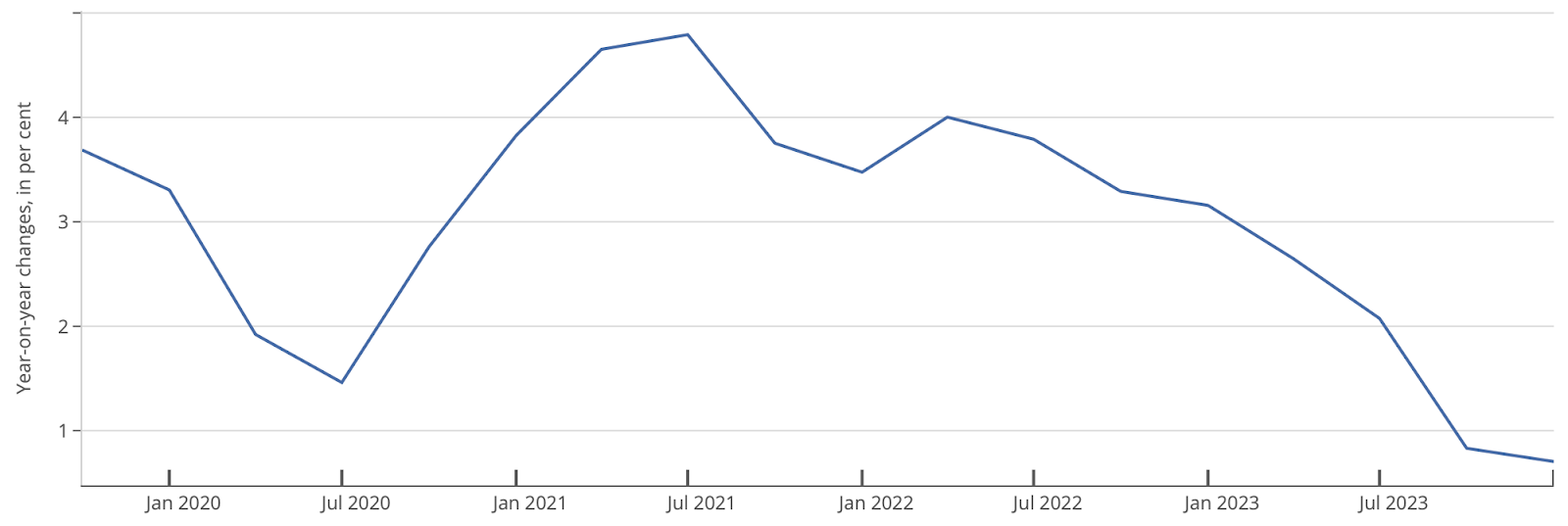

Selected residential property prices, Nominal, Year-on-year changes, in %

Source: (BIS)

Financing Requirements

Getting a loan requires more than just showing up at the bank. Lenders look closely at your credit score, debt-to-income ratio, and the down payment you can make.

A strong credit history opens doors to better mortgage rates and terms. Your debt-to-income ratio tells lenders if you can handle more debt responsibly. For most loans, a bigger down payment is usually needed compared to primary residences.

From personal experience, securing financing demands detailed planning and preparation, I once had to gather proof of steady income through tax returns and salary slips to demonstrate my ability to repay the loan.

Also, having cash reserves set aside convinced the lender I could cover unexpected costs or vacancies. Investment success hinges on understanding these financial prerequisites thoroughly before applying for any kind of mortgage loan or approaching hard money lenders for funds.

Comparing Home Equity Loans and HELOC for Investment Financing

Securing the right financing can make a huge difference in your journey as an investor. You have options like equity loans and Home Equity Lines of Credit (HELOC) at your disposal. Both can fund your investment, but they work differently. Let's break down these options so you can make an informed choice.

From firsthand experience, I've found that understanding these differences is key. It gave me a predictable payment schedule, which was perfect for a big project with a defined cost. On the other hand, a HELOC suited me later when I needed flexible access to funds over a few years for ongoing property improvements.

Each option has its place, depending on your investment strategy and financial situation. Comparing the short- and long-term costs, and considering how you plan to use the funds, will guide you to the right choice. Remember, with both options, your property serves as collateral. Ensure you have a solid repayment plan to protect your investment.

Strategies for Acquiring More Properties with Existing Mortgage Loans

You want to grow your real estate portfolio. Using existing mortgage loans smartly can make this easier. Here are ways to do it:

- Leverage Equity: Use the equity from one property to finance another. This means if you own a part of your residence outright, you can borrow against it to buy more properties.

- Refinance for Better Terms: Sometimes refinancing an existing loan gives you lower rates or better terms, freeing up cash that you can invest in new properties.

- Apply for a HELOC: A line of credit works well for investors. It lets you borrow money as needed, using your current property as security.

- Consider Seller Financing: This involves making payments to the seller instead of a traditional lender, which can be easier and faster than standard loans.

- Use a Property Manager: Hiring someone to manage your properties frees up time and might make lenders more willing to work with you since it shows professional management.

- Explore Government-Backed Loans: Some programs offer favorable terms for investors willing to buy and improve residential buildings, and then rent them out.

- Bundle Mortgages: Combining several mortgages into one can reduce fees and simplify payments, making finances easier to handle as you grow your investments.

- Invest in Diverse Locations: Properties in different areas spread risk and might catch the eye of lenders interested in geographical diversity in their portfolios.

Each strategy requires careful planning and understanding of the financial markets and real estate investment climate. Keeping abreast of changes in mortgage rates, property values, and market trends is crucial for success.

Conclusion

Securing loans opens doors to earning a good return, picking the right loan, and understanding its terms well. This guide showed options like bank mortgages and private lenders.

Each has its benefits, use this knowledge to grow your investments wisely.

FAQs

1. What is an investment property?

It is a real estate property purchased to earn a return through rental income, capital appreciation, or both.

2. How can I apply for a home loan?

To apply for a home loan, you typically need to have a good credit score, stable income, and necessary documents like proof of income, identification, and financial statements.

3. What are the key factors influencing interest rates on property finance?

They are influenced by various factors including economic conditions, central bank policies, inflation rates, and the borrower's creditworthiness.

4. How can I become a successful property investor?

Becoming a successful property investor involves thorough research, financial planning, understanding market trends, and building a diversified portfolio of properties.

5. What is the concept of buy-to-let properties?

Buy-to-let properties are purchased with the specific purpose of renting them out to tenants to generate an income stream for the investor.

6. How can I improve my affordability?

Improving affordability can be achieved by increasing your income, reducing expenses, enhancing your credit score, and exploring financing options.

7. What should I consider before choosing a tenant for my property?

Before selecting a tenant for your property, it's essential to conduct thorough background checks, verify references, and ensure the tenant's financial stability.

8. How can I invest in property with finance?

By securing finance through banks, financial institutions, or specialized lenders to fund the purchase or development of properties.

Author: Currie Group